The end of quantitative tightening may not be the market boost it appears to be

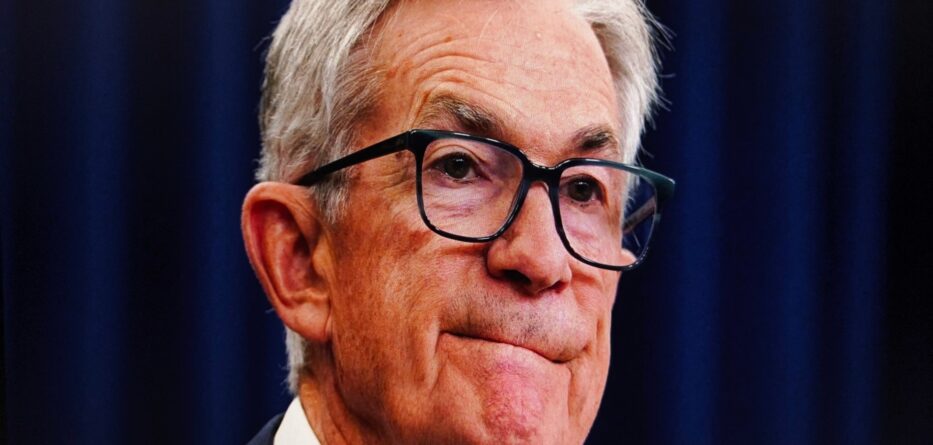

Federal Reserve Chair Jerome Powell just announced that the Fed will soon end its balance sheet reduction program, better known as quantitative tightening (QT). The move signals a major policy shift after more than three years of draining liquidity from the financial system. But while investors may cheer the end of QT, history offers a sobering reminder: this kind of “good news” often comes just before the storm.

Since June 2022, the Fed has reduced its balance sheet by $2.2 trillion in an effort to curb inflation and cool the economy. Conventional wisdom suggests that halting QT should benefit equities since more liquidity could flow into risk assets. Yet the data tells a different story. Over the past two decades, the stock market has actually performed better during periods of QT than during times of quantitative easing (QE).

During this most recent tightening phase, while liquidity was being pulled from the system, the S&P 500’s total return index rose at an annualized rate of 20.9 percent, nearly double its long-term average. Looking further back, since 2003, the index has gained an average of 16.9 percent during 12-month periods when the Fed’s balance sheet was shrinking, compared to 10.3 percent when the Fed was expanding it.

The reason for this counterintuitive pattern lies in timing. The Fed typically turns to QE when the economy is in trouble, injecting liquidity to stabilize markets. But because policy effects take time, these expansions often occur during recessions or downturns, when stocks are already under pressure. The Global Financial Crisis in 2008 and the pandemic lockdown in 2020 both saw massive balance sheet expansions — and equally severe bear markets.

By contrast, the Fed tightens when the economy is strong, as it did over the past few years. QT has coincided with growth and resilience, not weakness. That makes Powell’s announcement potentially worrisome. If the central bank now feels the need to stop tightening, it may be seeing early signs of economic slowdown.

In other words, the end of QT is less a celebration and more a signal. The Fed may be preparing for a softer economy in 2026, one that could test the market’s recent optimism. Stocks might rally briefly on the headlines, but as history shows, these transitions rarely come without turbulence.

Investors should take Powell’s pivot as a cue to stay cautious, not euphoric. If history repeats itself, things could get worse before they get better.

-

Credit: Shutterstock When Albert Einstein reportedly called compound interest the “eighth wonder of the world,” he wasn’t talking about...

Credit: Shutterstock When Albert Einstein reportedly called compound interest the “eighth wonder of the world,” he wasn’t talking about... -

Credit: Shutterstock In a dramatic and decisive operation, Mexican Special Forces have dealt a historic blow to organized crime,...

-

Credit: Shutterstock Former President Barack Obama proved Sunday night that his reflexes — and his love for the game...

-

Credit: Shutterstock If “Trump Accounts” weren’t on your radar before, they probably are now. After a high-profile Super Bowl...

-

Credit: Shutterstock While the Super Bowl delivered its usual edge-of-your-seat action on the field, millions of fans made a...

-

Credit: Shutterstock The U.S. Department of Justice on Friday unveiled its most extensive disclosure yet in the Jeffrey Epstein...

-

Credit: Shutterstock Gold prices surged to a historic high this week, crossing the $5,300 per ounce threshold as strong...

-

Credit: Shutterstock In a dramatic reset aimed at cooling tensions, Border Czar Tom Homan has ordered Border Patrol leadership...

-

Credit: Shutterstock Bitcoin, the world’s largest cryptocurrency, has stumbled below the closely watched $89,000 level, reminding investors just how...

-

Credit: Shutterstock Bitcoin is back in the spotlight — and it’s making waves. The world’s largest cryptocurrency surged past...

-

Credit: Shutterstock Former President Donald Trump has once again ignited global controversy—this time by reviving his push for U.S....

-

Credit: Shutterstock Gold is having a moment — and it’s a big one. As global uncertainty rattles markets, gold...